General Discussion

Related: Editorials & Other Articles, Issue Forums, Alliance Forums, Region ForumsI've lost more that 10% of my savings in less than a week!

Thank you Dementia Donnie!

= new reply since forum marked as read

Highlight:

NoneDon't highlight anything

5 newestHighlight 5 most recent replies

= new reply since forum marked as read

Highlight:

NoneDon't highlight anything

5 newestHighlight 5 most recent replies

Shellback Squid

(10,068 posts)

bif

(26,967 posts)I try to talk to my broker as little as possible because he's a tRumper and he can be a real pain in the ass. But he's fiscally conservative and I've done well by him. I think I'm just going to ride this one out.

I have the most conservative position I can have so.... same.

Ms. Toad

(38,575 posts)We're on the same page (financially and politically). He knows I'm not looking to withdraw next week - and that I know the market goes up and down. When I first transferred the money from the crappy money guy my spouse uses I'd get a call or email anytime there was market turmoil - just to make sure I wasn't panicking. Now he knows to spend his time on other clients.

Emile

(42,171 posts)

WhiskeyGrinder

(26,906 posts)bif

(26,967 posts)Stocks and mutual funds.

Groundhawg

(1,217 posts)Shellback Squid

(10,068 posts)

EdmondDantes_

(1,746 posts)Over time the market goes up. You still own whatever amount of shares and over time they are exceedingly likely to rebound. Panic selling isn't a good idea unless you absolutely need the money, which your investments probably shouldn't be your rainy day fund.

If you are close to retirement, you probably shouldn't have nearly as much invested in stocks because of short term volatility.

stopdiggin

(15,402 posts)that assets are no longer mine TODAY ...

(I think your comments were well intentioned ... but it is a mistake to minimize another's losses )

ProfessorGAC

(76,613 posts)There have been multiple instances, in the last 40 years, where a precipitous drop in the markets caused losses in retirement account savings that were not fully recovered.

For instance; Black Friday 1987. 20% drop in value. The rebound took 18 months to fully recover. Now at that point investors had what the had 18 months prior, but that is not full wealth recovery.

If a person had $1 million, then lost 20% to $800k, over the next 18 months, they recovered the $200k.

But then, at 8.5% per year at the 10 year point, they would have $2 million.

Absent the crash, the $1 million at 8.5% for the full 10 years results in investment growth to $2.26 million.

That's $260,000 said investor will never have.

And this example includes a 25% recovery in only 18 months, which is an annualized 16.7% return.

It's simply untrue that wealth is not lost in the long term.

Drops like this typically result in wealth never realized even though the absolute value does go up.

bif

(26,967 posts)

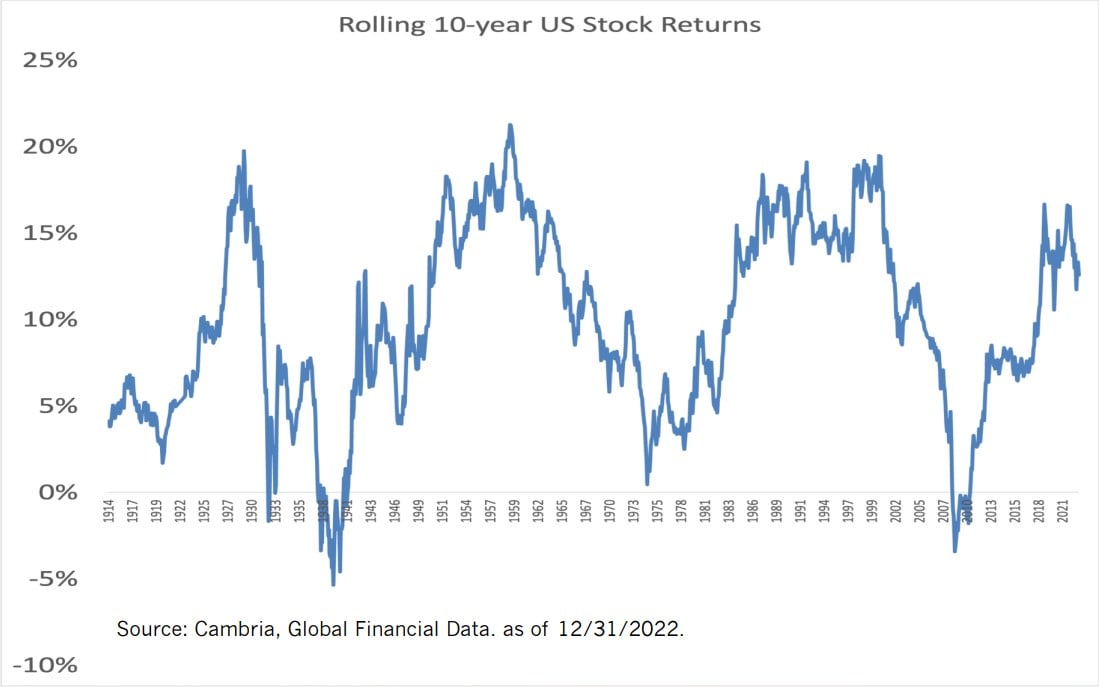

PoindexterOglethorpe

(28,493 posts)Meanwhile, this chart may be useful:

ProfessorGAC

(76,613 posts)...many, many times.

It changes nothing about the notion that, unless there are multiple over-forecast increases, it is possible, even likely, that at the terminus of a long range plan, there will be a deficit of accumulated wealth.

Not sure how you think that chart is relevant to the point.

PoindexterOglethorpe

(28,493 posts)thanks to my wonderful financial advisor. And that includes my taking out about 4% each year. You seem to be projecting long term losses in a rising market. Really? So what is my guy doing that is wrong here?

Plus, falling markets are a good time to invest. Small investors, day traders, simply buy and sell too frequently.

ProfessorGAC

(76,613 posts)I provided a clear example.

I'm saying nothing of the sort that you inferred.

Not sure where your conclusion came from.

My example showed a RISE in overall wealth.

You seem so bent on making a point that you didn't even go through the example.

stopdiggin

(15,402 posts)Last edited Fri Mar 14, 2025, 01:08 AM - Edit history (1)

the fact that the markets rise and fall - in no way precludes the chance of real loss ...

Kind of surprised we have so many posts willing to weigh in - - - To the effect, assuming the OP either 1) did something wrong to incur losses - or 2) didn't understand his real financial position

muriel_volestrangler

(106,133 posts)It's far larger than GDP growth unless you pick the the right country every single year.

I'd never advise anyone to expect long term 8.5% growth.

We don't know the precise mix of stocks the OP is in (but indices themselves have not dropped 10% in one week - they've done worse than most of the market). So we don't know when they had previously gained the 10%.

For instance, the S&P 500 is currently 4.5% below its high for the week, and is back to the level of 27 weeks ago. It's not nice (and shows the market now realises it was foolish to think Trump would be good for it), but still 15.7% above its peak in Dec 2021. That's a respectable 4.6% pa growth - above a peak.

The point is that the level of their stocks a week ago was snapshot of what turned out to be a bubble - unrealistic.

ProfessorGAC

(76,613 posts)The S&P has gone up at 7.98%, inflation adjusted, for the last 30 years. 107% unadjusted for inflation.

So yes, the 8.5% was a guess on my part, and you can call it arbitrary.

But, it doesn't matter what the DCF rate is. Only the delta changes.

At a lower ROI, the "lost" wealth is smaller, but still money an investor never gets.

If the rate is higher than 8.5%, then the delta goes up.

"Bubbles" don't change the math. And, since the long range return is based on some historical average, and I used a 10 year, not 10 werk or month timeframe in my example, short term corrections can happen but still not change the math.

The point is, that a sudden fall in value can indeed result on a loss of potential wealth at the end of a long investment.

The post to which I was replying said the drop (or to use your concept, correction) didn't really cost the OP anyway.

I provided a historical example that refuted that.

And your point of when the 10% rise or fall happened is not germane to the long term overall return.

This is a pretty straightforward financial concept. And, long accepted as fact. I'm not getting why anyone would pushback.

BTW: Your 4th paragraph actually reinforces my point. Why stocks go up or down is not relevant to the math.

muriel_volestrangler

(106,133 posts)There is no expectation of a certain growth from an arbitrary point (such as "the beginning of this week" or "the start of August 1987" ). It's pointless to take a moment in time and then say "my arbitrary growth should start from that moment". Now, that is a pretty straightforward financial concept. Now you've called it "potential wealth" rather than "wealth", I think you've admitted this Your example was not "historical", it was hypothetical.

Why stocks go up or down may not be relevant to your math, but it is relevant to investing, and more relevant than your hypothetical math.

stopdiggin

(15,402 posts)I'm really surprise there is this amount of pushback on what is really pretty basic fundamentals

Ms. Toad

(38,575 posts)Whether or not you need the money. My spouse hits mandatory withdrawals in April, based on December valuation.

stopdiggin

(15,402 posts)smug (and quite clueless) know-it-alls

NO - my ever so wise and good friend - I am actually 10% poorer today than I was ...

Ms. Toad

(38,575 posts)Groundhawg

(1,217 posts)nitpicked

(1,795 posts)I partially bailed out in 2026 and went into securities.

In 2009, it looked like the right thing.

Even, to my view, for several years.

BUT then, after late 2022, the market was IMO shot full of "hopium" and the S&P went up 50% or more.

Even Musk took over a failed dealership in my county to peddle his csrs..

IMO, a correction was overdue.

But when it strikes can impact one's plans.

bif

(26,967 posts)

Miguelito Loveless

(5,723 posts)into an interest bearing cash account before the inauguration. I have avoided losing about $10,000 so far.

PoindexterOglethorpe

(28,493 posts)until such time as you sell for less than what you paid. And over time the stock market goes up. And up.

I have a wonderful broker who has done very well for me over the years. I am steadily taking out some 4% of my money each year, and each year (for the past 20 with him) my money has gone up.

Ishoutandscream2

(6,783 posts)This shit didn’t have to happen!

Ms. Toad

(38,575 posts)Just don't look.

My spouse is going to be hurting. She's got to start taking mandatory withdrawals from her IRA in April - based on the market valuation 12/31. Ugh.

kelly1mm

(5,756 posts)fully fund my IRA/Spousal IRA and SEP plan all in one lump sum (about $25k annually) in the beginning of April for the previous year deductions. So this is good timing for me.

bucolic_frolic

(55,022 posts)There are big blocks being unloaded, in AI and Tech.

Growth stocks have been hit hard because of the predicted coming recession. Mid-cap growth whacked. Mid-cap value not so much. Foreign funds not much at all at least the ones i watch. Indexed whacked. I'm a queer duck but I like managed funds if they're not a reservoir for the Mag-7. Obscure niche funds can hold their own while managed funds essentially trying to add alpha by holding tech get pricked.

3 years worth

JT45242

(4,027 posts)And the accounts recovered --

This may be different as Mango Mussolini and Apartheid Clyde rush us towards a world war and/or an economic depression.

I am 54 and need the accounts to revover and long term grow for me to be able to retire in my early to mid sixties.

I am not looking daily, but am considering switching some assets into a metals IRA in gold/platinum/etc to try to mitigate some of these losses.

But I am at an age that I am still looking at 10ish years out and not taking out money when my retirment accounts could be low.